FX BASKET QUANT is our third portfolio trading strategy. The strategy

started live trading on January 1, 2013. The actual performance is tracked on the Performance page of our web site.

FX BASKET

QUANT

-

HYPOTHETICAL PERFORMANCE REPORT FROM STRATEGY BACK TESTING

PLEASE READ

FIRST DISCLAIMERS AT THE

BOTTOM OF THIS PAGE

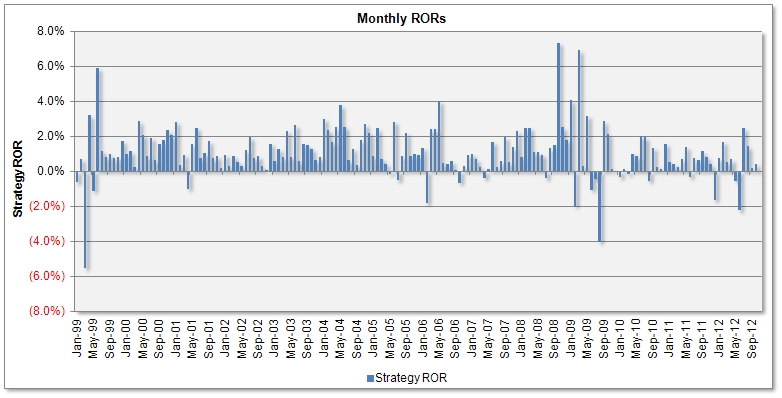

1. Monthly Rates

of Return (ROR), Before Performance Fees

Daily rates of return (ROR), from strategy

back testing, can be downloaded from this Excel spreadsheet.

Results are net of spreads and commissions and before performance

fees.

PAST

PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

2. Performance

Analytics - FX Basket Quant (Before Performance Fees)

Strategy Returns (Before

Performance Fees)

Testing

period

Jan 1999 - Dec 2012

Net profit on fixed capital

with / without monthly profit reinvesting

Average number of R/T transactions

(100k FX lots) per $1Million NAV per year

-

Average annual transaction costs -

bid/ask spreads (deduct from annual ROR)

2.5%

Average transaction bid/ask spread,

as a fraction of the transaction value

0.0002

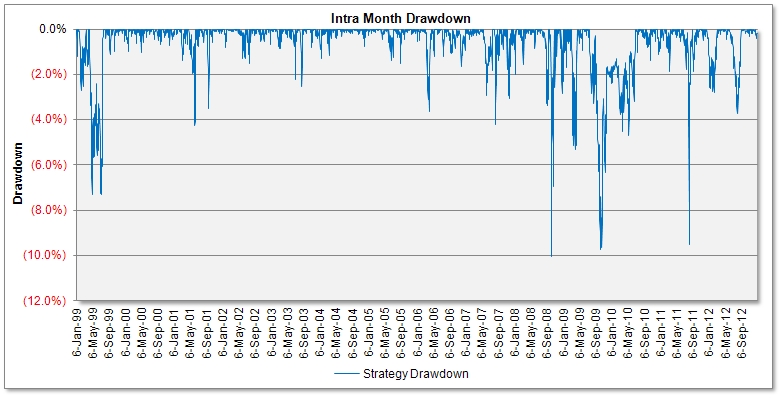

3. Performance Graphs and Histograms

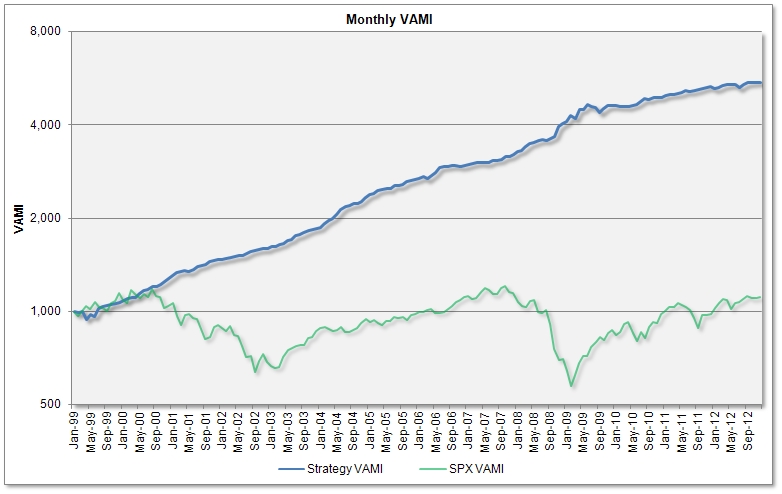

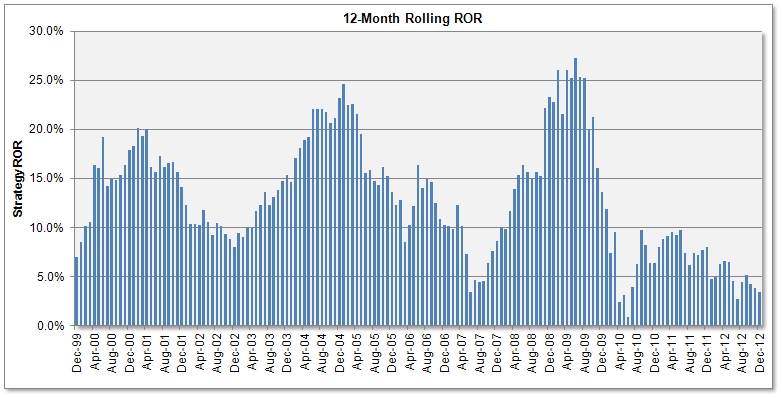

3.1 Monthly Graphs

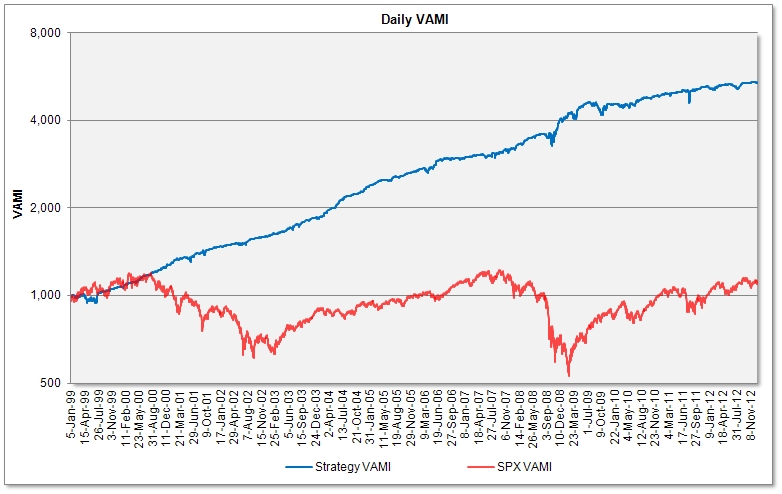

3.2. Daily Graphs

Better

results (smaller drawdown and better Sharpe and Sortino Ratio) can be

obtained by trading multiple trading strategies. The three currency trading

programs (FX Quant 11, FX Index Arb and FX Basket Quant) can be further

combined with our volatility

trading programs -

see this 6-strategy composite

back testing report.

HYPOTHETICAL OR

SIMULATED PERFORMANCE RESULTS HAVE CERTAIN INHERENT LIMITATIONS. UNLIKE AN

ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING.

ALSO, SINCE THE TRADES HAVE NOT ACTUALLY BEEN EXECUTED, THE RESULTS MAY HAVE

UNDER-OR-OVERCOMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH

AS LACK OF LIQUIDITY. SIMULATED TRADING PLATFORMS IN GENERAL ARE ALSO SUBJECT TO

THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION

IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES

SIMILAR TO THOSE SHOWN.

Risk Disclaimer

THE RISK OF

LOSS IN TRADING COMMODITIES CAN BE SUBSTANTIAL. YOU SHOULD THEREFORE CAREFULLY

CONSIDER WHETHER SUCH TRADING IS SUITABLE FOR YOU IN LIGHT OF YOUR FINANCIAL

CONDITION AND INVESTMENT OBJECTIVES. PAST PERFORMANCE IS NOT NECESSARILY

INDICATIVE OF FUTURE RESULTS. THE PERFORMANCE QUOTED REPRESENTS PAST PERFORMANCE

AND CURRENT PERFORMANCE MAY BE LOWER OR HIGHER. TRADING IN FOREIGN EXCHANGE IS

SPECULATIVE AND MAY INVOLVE THE LOSS OF PRINCIPAL; THEREFORE, FUNDS PLACED UNDER

MANAGEMENT SHOULD BE RISK CAPITAL FUNDS THAT IF LOST WILL NOT SIGNIFICANTLY

AFFECT ONE'S PERSONAL WELL BEING. THIS IS NOT A SOLICITATION TO INVEST AND YOU

SHOULD CAREFULLY CONSIDER YOUR FINANCIAL SITUATION PRIOR TO MAKING ANY

INVESTMENT OR ENTERING INTO ANY TRANSACTION. PLEASE SEE THE COMPLETE DISCLOSURE

DOCUMENT.