It took some time within

investment circles for currency to be recognized as something where one can add value. In currency markets,

because wherever there is a buyer there is a seller, it is said that currency markets are a

zero-sum game. Also, as the currency market is the most liquid and largest financial

market in the world, it is a big ocean to feed in. This allows opportunities for our

system to extract value from price noise and generate positive

returns.

Fx Quant 11, our quantitative currency

trading program, is based on

quantitative analysis - a statistical trading concept. It is based on

digital signal processing - DSP (to extract profit from high frequency price

noise), trend following (to profit from price trends) and position size management

(to limit exposure and risk). Unlike most trading systems, which attempt

to predict market direction, our trading model reacts to price action and

makes trading decisions. We believe that guessing market direction is

impossible, at least so say noble guys

with Nobel prizes.

Diversification. One of

the most important aspects of our trading program is diversification, the

ability to trade several different currencies. The strategy creates a

complex portfolio of 11 global currencies and adjusts its components daily.

The emphasis is on currencies of developed countries (G10 currencies), but current and

future portfolio construction is at Quant Trading's discretion (currently,

FX Quant 11 trades 9 currencies against USD). In fact, the

strategy generates signals based on combinations of 4-th class of all

available currency pairs based on the 11 base currencies. For example, one

such combination can be NZDCAD+GBPNOK+CHFAUD+EURSEK etc. The total number of

these combinations, i.e. artificially created trading instruments, is

720,720. The mathematics of portfolio diversification

show that when weakly correlated trading instruments are combined together,

a higher risk adjusted return is generated (better Sharpe and Sortino Ratio) than with individual currencies. In other

words, diversification of currencies/instruments can lead to better

risk-rewards for the combined portfolio. For example, in a portfolio comprised of

only three instruments, one position

can be unprofitable at the moment, but the other two can show profits to more than

compensate for the losses incurred with the losing one.

Our system works with arbitrarily selected currencies. We decided to stay with currencies of

developed countries (EUR,

USD, GBP, CHF, JPY, CAD, NZD, AUD, SEK, NOK, DKK and SGD) for their excellent liquidity and tight bid/ask spreads. The system is

non-parametric (it has zero degrees of freedom), i.e. there are no parameters to optimize.

The annualized

rate of return and drawdown are controlled by adjusting the mean system leverage.

This makes the system very robust, i.e. it does not depend on various price patterns (which most trading systems

depend on).

Uniqueness

and profitability of

the FX Quant 11 trading program.

In contrast to other trading systems, our

strategy is not pattern-based, simple trend-following or counter-trend trading

system. Our research shows that most profit opportunities in Forex come from

noise trading. Talking technical trader's language, this is something like

counter trend trading with gradual stops. To catch these fast price variations,

FX Quant 11 makes use of digital filtration. During periods of pure and

prolonged price trends, the strategy uses a trend following module, in attempt

to catch these longer term trends.

Due to the excellent

diversification, the combined leverage (the value of all currencies held long,

against those held short, relative to NAV - Net Asset Value) oscillates around its mean and rarely reach the

maximum of 20 (this is another important system's feature).Our

numerical simulations show that in long run, and if a reasonably high

average leverage is used, the profit factor (profit-to-loss ratio) of our system will be greater than unity (the sum of gains will

always be greater than the sum of losses). The mean leverage is carefully determined in order

to avoid disastrous drawdowns.

Our standard risk parameters

employ an average combined leverage (the long positions value relative to net

asset value) around 0.42 for the entire portfolio. The

maximum leverage is currently limited to 2:1.

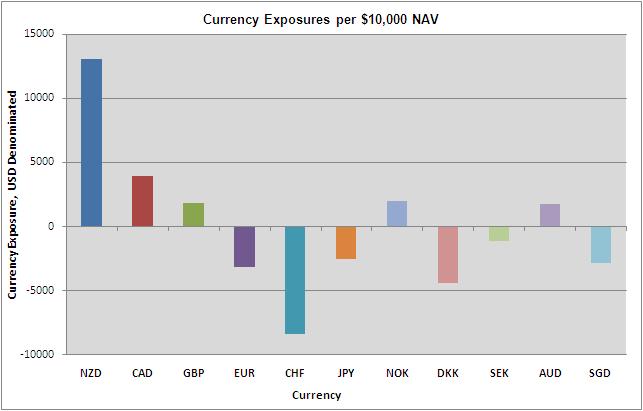

The system opens positions in opposite,

long/ short directions for various currencies. It is USD neutral (i.e. USD

amount bought = USD amount sold), but there is a long/short exposure in other

currencies - see these position size graphs. As

stated before, due to portfolio diversification, the risk is more limited than

if just one currency was traded alone.

Make sure you understand the

level of risk involved in the FX Quant trading strategy and ensure that it is suitable to your personal investing goals,

time horizons, and risk tolerance. The leverage used is a double sided sword: it improves

returns, but it also increases the risk. As with any investment, higher

potential return means higher risk. Drawdown and

value-at-risk (VaR) data and graphs for the currently used strategy can be found

in the Fx Quant 11 page of this web site.

Risk control is achieved

through a variety of means which in most market conditions should minimize

drawdowns. The first is portfolio construction and diversification;

second is controlling leverage through position sizing adjusted according

to account size, volatility and risk-reward analysis; and third is stops

based on money management rules. The main risk control mechanism uses

diversification and position size management. The system rebalances portfolio by gradually

buying/selling fractional (odd sized) currency lots. Since the system

does not sharply open large positions in any currency, directional risk is

diversified among multiple currencies. As said

before,

the leverage oscillates around a long term average and the system does not

normally use

classical protective stops (unless a huge drawdown of 25% magnitude ever hits). When a

normal drawdown occurs, portfolio is rebalanced and the strategy continues

normal trading. The highest risk for the strategy is when prices of

multiple currency pairs move sharply, with little price noise, for a prolonged

period. To have some idea on the risk, please see the Drawdown graph in section

3.2 of the Fx Quant 11

page. The VaR (Value at Risk) concept is based on back testing and there is no guarantee the drawdown

will not be exceeded going forward. Although strategy drawdown never

exceeded 12% in back testing, a gradual stop-loss (strategy

de-leveraging) will be applied if drawdown ever exceeds 25%.

Drawdowns typically occur

when when volatility suddenly jumps following a period of calm market, in

combination with higher correlation between currencies. Such periods tend to be less frequent these days

(although there is no guarantee!), as the Forex market becomes more and more efficient - the "matured" G-7 currencies

particularly. Again, this is not to say that the market can not change its behavior

at any time!

As soon as market enters a consolidation phase with more price noise (actually, there is

always some noisy/random price action, even in a trending market), the system recovers

from losses and sets a new equity peak. This makes our system superior over most

rule-based, pattern recognition, Elliot Wave, W.D. Gann, many indicator-based trading

systems and other trading alchemy. No one knows if and when will the market change its behavior

and those systems will break up. Potential risk for our strategy comes from over-leveraged

trading, i.e. trading too large positions for the given account size. In

order to avoid a potential disaster, we keep the mean leverage around 0.42 (maximum

of 2.0).

You can see the back testing report of the latest trading strategy on the

Fx Quant 11 page of our web site.

For best results (smaller

position adjustments and minimum price slippage), the strategy trades odd-sized lots (Oanda has a 1

currency unit minimum dealing size). As a rule of thumb, the minimum account

size should be at least 10 times larger than lot size (a $100,000 account can trade

mini sized/10k lots and a $1,000,000 account can trade

regular/100k currency lots).