Below are given

back testing results of FX Quant 11 (ver. 12/2012), generated by our

software. These results should be considered as extrapolation into the past of

FX Quant 11 - Currency Trading Program, which started live trading on January 2, 2013. It replaced

the older versions of the strategy, which have

been trading since November 1, 2008. Performance fees (20% of

new net profit above high water mark) are not deducted from back testing results.

To see actual trading results, please go to the FXQ

/ Real Performance page.

FX Quant 11 features:

- The variability of returns is low and the

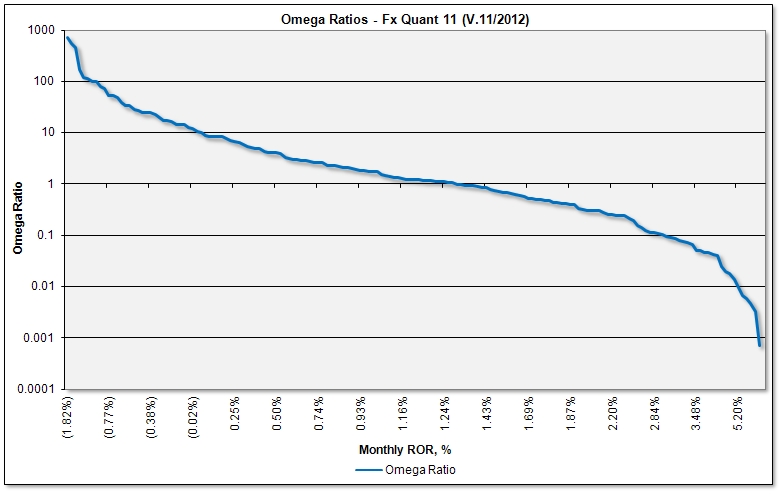

Sharpe, Sortino, Calmar and Omega Ratios are excellent - among the highest in

the currency trading industry. The strategy is extremely robust i.e. insensitive

to parameter changes (it is not a curve fitted, or over optimized system), which usually promises excellent

performance in forward trading, after the back testing period.

- Transaction costs are very low (2.45% of net

asset value per annum), relative to average annualized rate of return (27.9% per

annum). Since bid/ask spread costs are around 10% of theoretical return, actual

rates of return are 90% of theoretical returns.

- There is no

upper limit on the account size. By trading more frequently (for example,

1/3 of account traded each 8 hours) the strategy can trade accounts of virtually

any size without performance degradation (it would be even improved, due to

time-factor diversification)

- The strategy is not affected by price

slippage (it trades in small increments, by market orders, only once a day). Hence, the actual trading results are very close to hypothetical

results. See "Transaction costs" above.

Average number of R/T transactions

(100k FX lots) per $1Million NAV per year

980

Average annual transaction

costs - bid/ask spreads (deduct from annual ROR)

2.45% of NAV

per annum

Average transaction bid/ask spread, as a fraction

of the transaction value

0.00025

* -

Total long/short position value is roughly 2 × strategy leverage. It is used

for portfolio turnover and costs calculations. Leverage (long only position

value) is used as a measure

of exposure.

To see more backtesting results,download this Excel table(Fx Quant

11 - V.11/2012). Explore all Excel worksheets (click the tabs at the bottom) and scroll down all

worksheets to see graphs and performance analytics. You can also download daily rates of returnfrom backtesting

(Excel, 1 MB), with 5 day VaR calculations and 5-day ROR histograms.

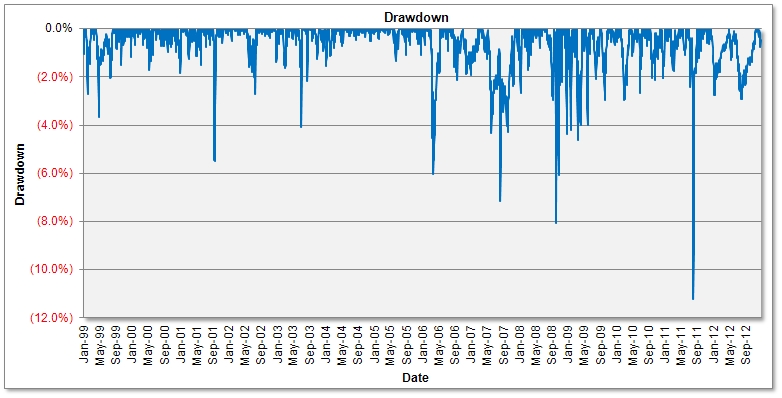

PLEASE ANALYZE AND

THOROUGHLY UNDERSTAND THE RISK / DRAWDOWN PARAMETERS ABOVE AND THE DRAWDOWN

CHART BELOW BEFORE YOU DECIDE TO INVEST IN THE PROGRAM. AS WITH ANY TRADING

PROGRAM, THERE IS NO GUARANTEE THE SYSTEM WILL NOT EXCEED THE WORST DRAWDOWN

FROM THE PAST. WE DO NOT RECOMMEND INVESTING MORE THAN 1/3 OF YOUR TOTAL

INVESTMENT PORTFOLIO IN ANY PARTICULAR PROGRAM, INCLUDING QT - CURRENCY

TRADING PROGRAM.

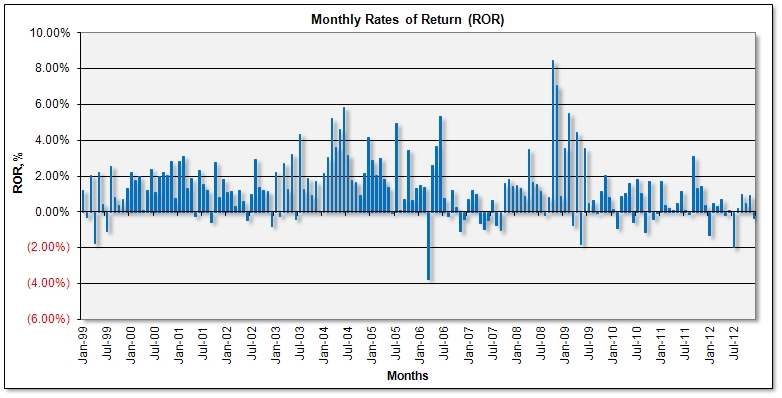

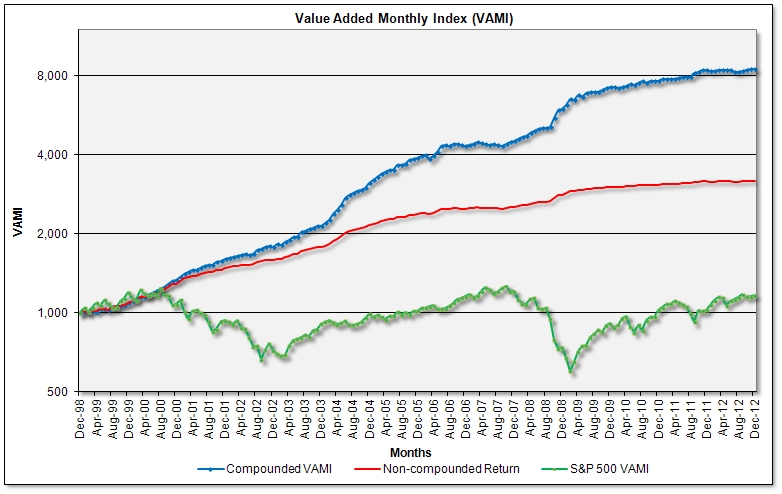

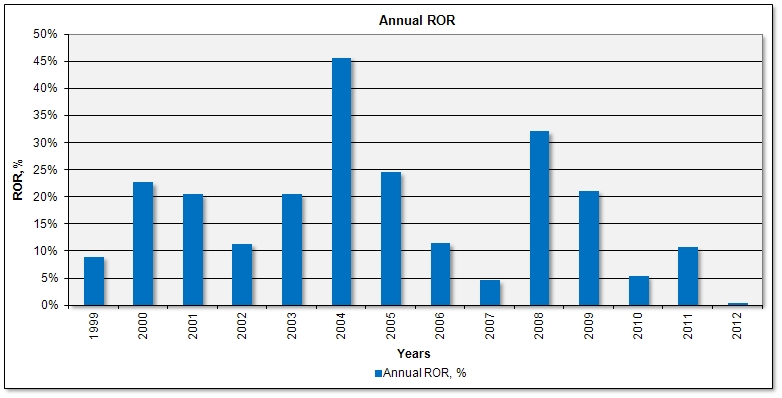

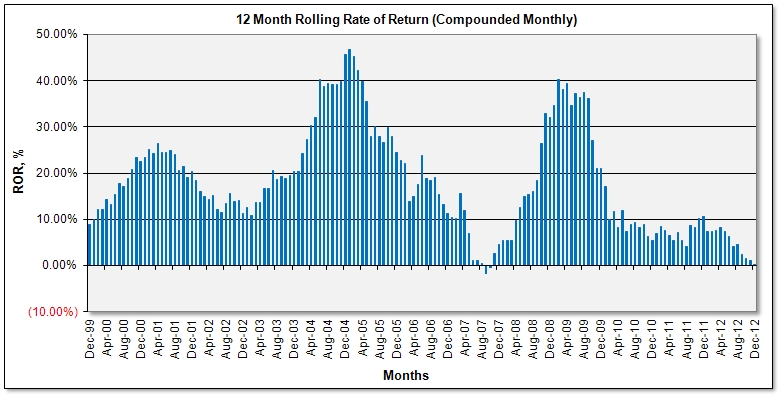

3. Performance Graphs and Histograms

3.1 Monthly Graphs

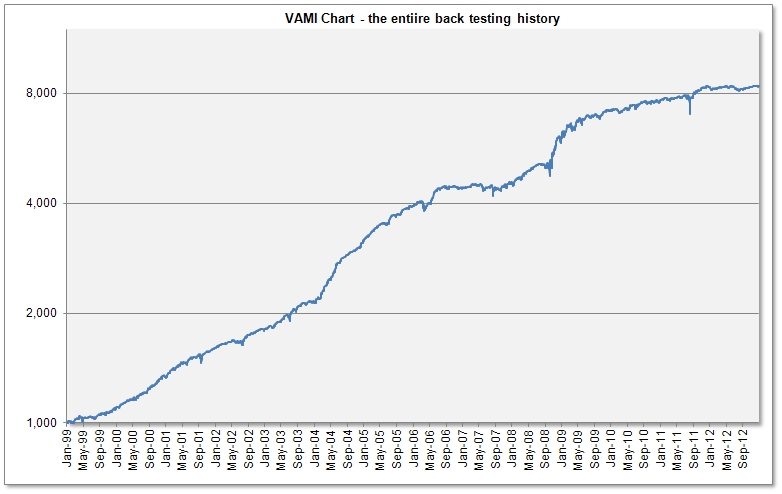

Note the semi-logarithmic co-ordinates in the

VAMI chart

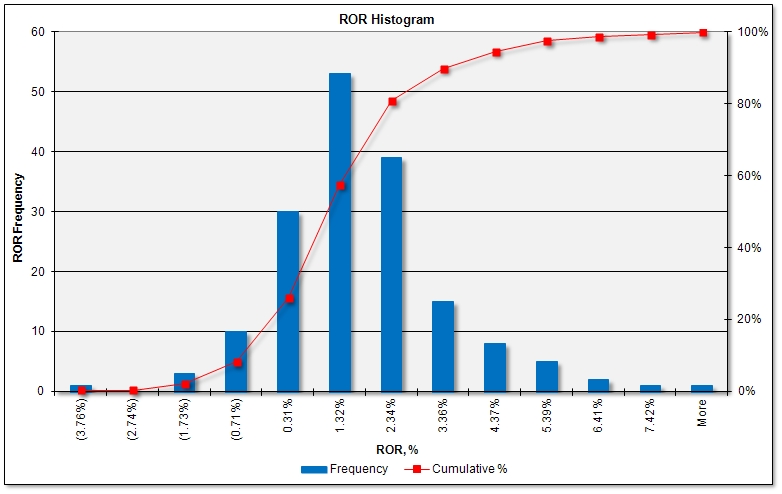

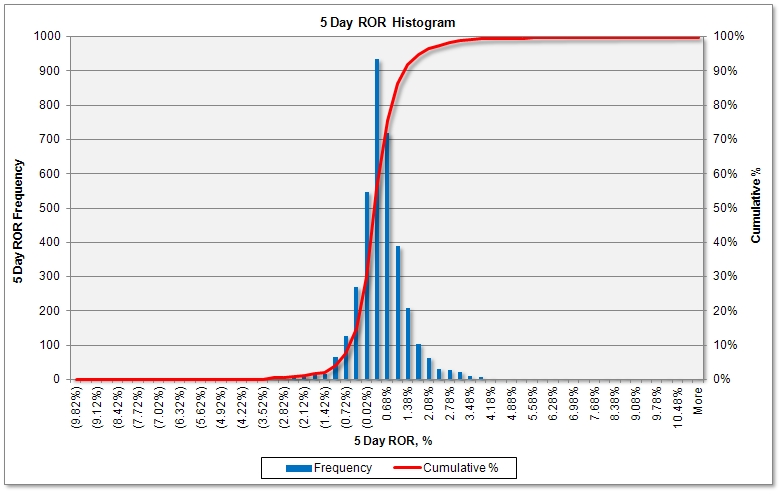

1. There is very regular,

bell-shaped, thin tailed distribution of 5-day rolling rates of return . Robust systems, which are not curve-fitted usually have

this type of distribution.

2. The 5-day rolling rate of

return (ROR) mean is positive and equals 0.299%. There is a 50%

probability that the 5-day rate of return will be greater than 0.299% and 50%

probability the return will be less than 0.299%.

3. 5-Day RORs are more clustered

in the positive territory in the histogram above. There is a 31.4% probability that a 5-day ROR will be

negative and a 68.6% probability the 5-day ROR will be positive.

4. The 5-day

Value-at-Risk (VaR)

for the 95% confidence level is 0.94%. This means that the risk of loss in a

5-day period is 0.94%, with a 95% probability. The probability of loss of more

than 0.94% in a 5 day period is 5%. Similarly, the 5-day VaR for the 99%

confidence level is 2.30%. Excessive negative RORs do and will happen, although

with decreasing probability. To see these calculations open the 5 Day ROR

Percentile tab in this

Excel workbook.

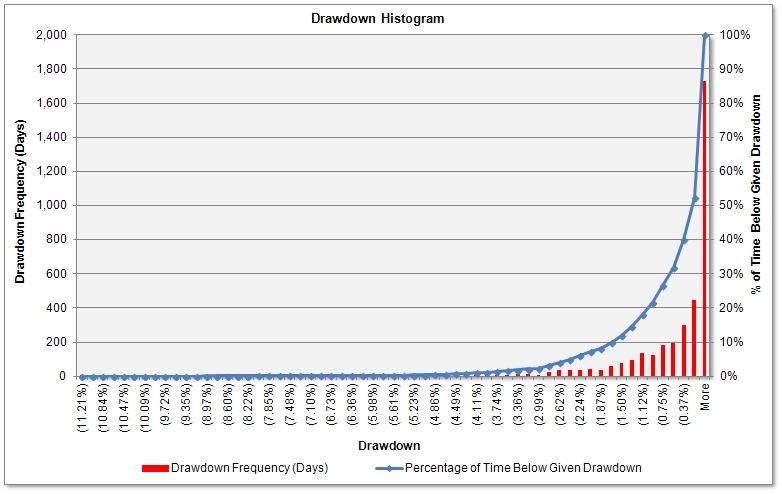

1.) how many days the system was in drawdown of

given magnitude (the red colored line).

The back testing period is 3638 days;

2.) what time (as a percentage of the total back testing time) the system

spent below a given drawdown level (the blue

colored line). For example, the system spent only 5% of time (182 out of

3638 days) in drawdown worse than

2.43%, and only 1% (36 out of 3638 days) in drawdown worse than 4.11%. These

figures also give some idea on the recovery time. Calculations can be found

in this Excel worksheet

(1.1 MB),

under the Drawdown Histogram tab.

The most important facts to remember from the

Drawdown Histogram are that:

1.) large drawdowns are relatively rare

(the larger the drawdown - the less the probability, although it does exist - see the

11.21% drawdown far left in the histogram above);

2.) the system

quickly recovers from extremely large drawdowns. There is no answer,

however,

how deep the drawdown can go; statistics only show it should not last for too long. This chart also shows

how important it is to be patient and not to quit trading during drawdown

(which is the worst possible moment to do so).

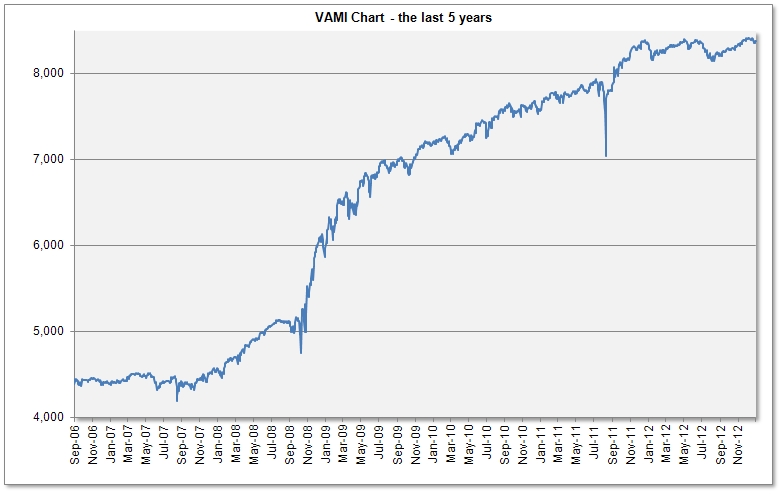

Compounding

(see the VAMI chart above)is an efficient method for increasing your account

equity exponentially, by reinvesting the profit

- try this

Financial Calculator.

Since FX Quant 11 trades in small increments, it is one of the few trading

programs suitable for monthly compounding. You can see these

formulas for ROR

calculations and compounding.

The above

tables and charts document FX Quant 11's historical hypothetical performance

based on back testing results. To see actual trading results, go to the

FXQ Real

Performance page (after January 1 , 2013).

Please note

that performance results reported are before performance fees, which

decrease returns. Interest on open positions is not taken into account in

hypothetical results. There are also slight differences in profit/loss at

different platforms, due to

different methods for profit/loss calculation (mark-to-market vs. closed

trade profit/loss).

Better

results (smaller drawdown and better Sharpe and Sortino Ratio) can be

obtained by trading multiple trading strategies. The three currency trading

programs (FX Quant 11, FX Index Arb and FX Basket Quant) can be further

combined with our volatility

trading programs -

see this 6-strategy composite

back testing report.

HYPOTHETICAL OR

SIMULATED PERFORMANCE RESULTS HAVE CERTAIN INHERENT LIMITATIONS. UNLIKE AN

ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING.

ALSO, SINCE THE TRADES HAVE NOT ACTUALLY BEEN EXECUTED, THE RESULTS MAY HAVE

UNDER-OR-OVERCOMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH

AS LACK OF LIQUIDITY. SIMULATED TRADING PLATFORMS IN GENERAL ARE ALSO SUBJECT TO

THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION

IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES

SIMILAR TO THOSE SHOWN.

Risk Disclaimer

THE RISK OF

LOSS IN TRADING COMMODITIES CAN BE SUBSTANTIAL. YOU SHOULD THEREFORE CAREFULLY

CONSIDER WHETHER SUCH TRADING IS SUITABLE FOR YOU IN LIGHT OF YOUR FINANCIAL

CONDITION AND INVESTMENT OBJECTIVES. PAST PERFORMANCE IS NOT NECESSARILY

INDICATIVE OF FUTURE RESULTS. THE PERFORMANCE QUOTED REPRESENTS PAST PERFORMANCE

AND CURRENT PERFORMANCE MAY BE LOWER OR HIGHER. TRADING IN FOREIGN EXCHANGE IS

SPECULATIVE AND MAY INVOLVE THE LOSS OF PRINCIPAL; THEREFORE, FUNDS PLACED UNDER

MANAGEMENT SHOULD BE RISK CAPITAL FUNDS THAT IF LOST WILL NOT SIGNIFICANTLY

AFFECT ONE'S PERSONAL WELL BEING. THIS IS NOT A SOLICITATION TO INVEST AND YOU

SHOULD CAREFULLY CONSIDER YOUR FINANCIAL SITUATION PRIOR TO MAKING ANY

INVESTMENT OR ENTERING INTO ANY TRANSACTION. PLEASE SEE THE COMPLETE

RISK DISCLOSURE.